4-3-2-1 Real Estate Budget Calculator

Your Financial Profile

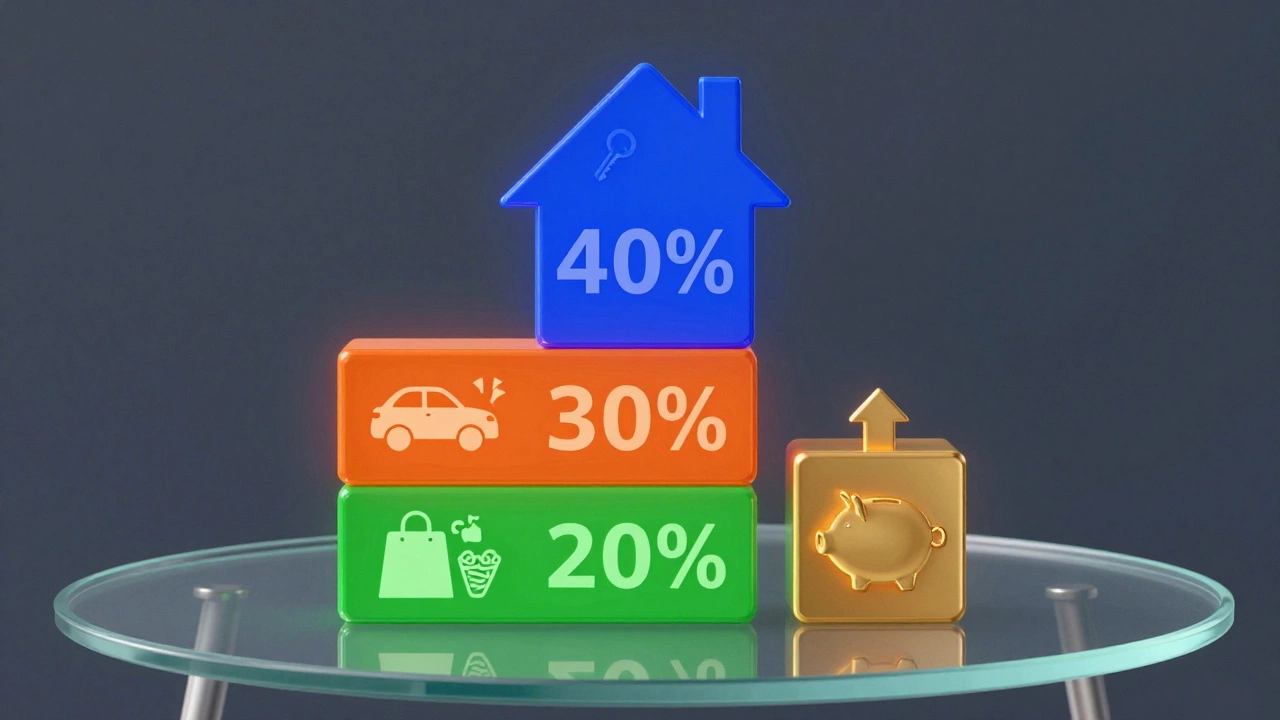

Quick Reference

- 40% Housing Expenses

- 30% Transportation

- 20% Personal Spending

- 10% Savings & Investments

Your 4-3-2-1 Budget Breakdown

Mortgage, insurance, taxes, maintenance

Available:

Car payments, fuel, insurance, maintenance

Food, entertainment, shopping, lifestyle

Emergency fund, CapEx reserves, retirement

Investment Recommendation

Rule Comparison

| Category | 4-3-2-1 Rule | 50/30/20 Rule |

|---|---|---|

| Housing | 40% | Up to 50% |

| Transport | 30% | Part of Needs |

| Personal | 20% | 30% |

| Savings | 10% | 20% |

The 4-3-2-1 rule is stricter on personal spending but prioritizes asset building through real estate investment.

Enter Your Income to Get Started

Calculate your ideal real estate budget using the proven 4-3-2-1 rule

You’ve found that perfect apartment or house. The photos are stunning, the location is prime, and your heart is racing with the idea of becoming a landlord. But before you sign anything, there’s a cold splash of reality waiting for you: can you actually afford it?

Many new investors rush into buy to let properties, often ignoring the fine print of their own finances. This is where the 4-3-2-1 rule comes in. It’s not a law written by any government body, but it is a widely respected heuristic used by savvy investors to keep their cash flow positive and their stress levels low.

This rule breaks down how much of your gross monthly income should go toward housing costs. It sounds simple, but applying it correctly can save you from financial ruin. Let’s look at exactly what those numbers mean and why they matter so much in today’s market.

Breaking Down the Numbers

The 4-3-2-1 rule divides your total gross monthly income into four distinct buckets. Here is the split:

- 40% goes to housing expenses (mortgage, insurance, taxes).

- 30% covers transportation costs (car payments, fuel, maintenance).

- 20% is allocated for personal spending (food, entertainment, shopping).

- 10% must be saved or invested.

At first glance, this might seem tight. After all, giving nearly half your paycheck to housing feels aggressive. However, when you are looking at investment properties, this ratio ensures that you aren’t over-leveraged. If your housing cost exceeds 40% of your income, you leave very little room for error if the tenant leaves or repairs pile up.

Why Housing Takes the Biggest Slice

In traditional personal finance advice, like the 50/30/20 rule, housing is often capped at 30%. But the 4-3-2-1 rule pushes that to 40%. Why the difference?

For an investor, housing isn't just a place to sleep; it's an asset class. By allocating 40% to housing, you acknowledge that building wealth through real estate requires significant upfront capital commitment. This percentage includes your principal, interest, property taxes, and insurance-often abbreviated as PITI.

If you are buying a home to live in, sticking to 30% is usually safer. But if you are treating this as a business venture, the 40% limit forces you to find properties that fit within a strict budget, preventing you from stretching too thin across multiple deals.

Transportation: The Hidden Cost

The next chunk is 30% for transportation. This is where many people get tripped up. We tend to think of transportation as just gas money, but it includes everything related to getting around. That means car loans, public transit passes, parking fees, and even regular maintenance like oil changes and tire rotations.

If you are managing rental properties, you will likely need to travel to inspect units, meet contractors, or handle emergencies. Keeping your transportation costs under 30% ensures that your mobility doesn’t eat into your ability to pay the mortgage on your investments.

Personal Spending and Savings

The final 30% of your income is split between living life and saving for the future. Twenty percent goes to personal needs and wants. This covers groceries, dining out, hobbies, and clothing. It’s your freedom fund.

The remaining 10% is non-negotiable savings. In the context of real estate investing, this isn’t just for retirement. This is your emergency fund for vacancies, major repairs, or unexpected tax liabilities. Without this buffer, one bad month can derail your entire portfolio.

Applying the Rule to Buy-to-Let Investments

When you apply the 4-3-2-1 rule to buy to let strategies, you have to adjust your perspective slightly. You aren’t just looking at your personal income; you are looking at the property’s potential income versus its costs.

However, the rule still applies to your personal cash flow. Before taking on a new rental property, ask yourself: "Does adding this mortgage payment push my total housing costs above 40% of my gross income?" If the answer is yes, you might be taking on too much risk.

Consider this scenario: You earn $8,000 a month. According to the rule, your maximum housing expense should be $3,200. If your current mortgage is $2,000 and the new rental property would add $1,500 in payments, your total becomes $3,500. That breaks the 40% ceiling. You’d need to either find a cheaper property, increase your income, or wait until you have more equity built up.

Comparison: 4-3-2-1 vs. Traditional Rules

| Category | 4-3-2-1 Rule | 50/30/20 Rule | Best For |

|---|---|---|---|

| Housing | 40% | Part of Needs (up to 50%) | Investors prioritizing assets |

| Transport | 30% | Part of Needs | Commuters with high transport costs |

| Personal | 20% | 30% (Wants) | Lifestyle flexibility |

| Savings | 10% | 20% (Savings/Debt) | Wealth building vs. debt payoff |

As you can see, the 4-3-2-1 rule is stricter on personal spending and savings compared to the popular 50/30/20 rule. This discipline is crucial for real estate investors who need to maintain liquidity while holding illiquid assets like property.

Pitfalls to Avoid

Even with a solid rule, mistakes happen. Here are common traps that trip up new landlords:

- Ignoring Vacancy Rates: Your 40% housing budget assumes full occupancy. What happens if the unit sits empty for two months? Factor a 5-10% vacancy rate into your calculations.

- Underestimating Maintenance: Old buildings break. Set aside part of your 10% savings specifically for capital expenditures (CapEx) like roof replacements or HVAC failures.

- Mixing Personal and Business Expenses: Keep your rental income and expenses separate. Using rental cash flow to cover personal grocery bills can lead to tax nightmares and cash flow gaps.

Final Thoughts on Financial Discipline

The 4-3-2-1 rule isn’t a magic wand. It won’t fix a bad property choice or a declining market. But it does provide a clear framework for decision-making. By keeping your housing costs to 40%, transport to 30%, personal spending to 20%, and savings to 10%, you create a balanced financial profile that can withstand the ups and downs of real estate investing.

Start by auditing your current budget. Where do you stand? If you’re already over 40% on housing, focus on paying down debt or increasing income before taking on another property. Real estate is a marathon, not a sprint. Play the long game, and the numbers will work in your favor.

Is the 4-3-2-1 rule suitable for first-time buyers?

Yes, but with caution. First-time buyers often have lower incomes and higher relative housing costs. If you cannot meet the 40% housing threshold without sacrificing essential savings, you may need to look for more affordable properties or consider co-buying options.

Can I adjust the percentages based on my lifestyle?

You can tweak them, but be careful. Reducing the housing percentage below 40% frees up cash but limits your purchasing power. Increasing personal spending beyond 20% reduces your safety net. Always ensure your savings remain robust enough to cover emergencies.

Does this rule account for property management fees?

Property management fees should be included in the 40% housing bucket. They are a direct cost of owning the property. Ignoring them will make your net returns look better than they actually are, leading to poor financial decisions.

How does inflation affect the 4-3-2-1 rule?

Inflation erodes purchasing power, meaning your fixed 10% savings might not grow as fast as prices rise. To counteract this, aim to invest your savings in assets that outpace inflation, such as diversified real estate portfolios or index funds, rather than keeping them in low-interest accounts.

What if my income varies month to month?

If you have variable income, base your budget on your lowest expected monthly earnings. This conservative approach ensures you can still meet your 40% housing obligation even during slow months. Use surplus income from good months to boost your 10% savings buffer.

Corbin Fairweather

I am an expert in real estate focusing on property sales and rentals. I enjoy writing about the latest trends in the real estate market and sharing insights on how to make successful property investments. My passion lies in helping clients find their dream homes and navigating the complexities of real estate transactions. In my free time, I enjoy hiking and capturing the beauty of landscapes through photography.

view all postsWrite a comment