First-Time Buyer Deposit Calculator

Calculate Your Home Deposit

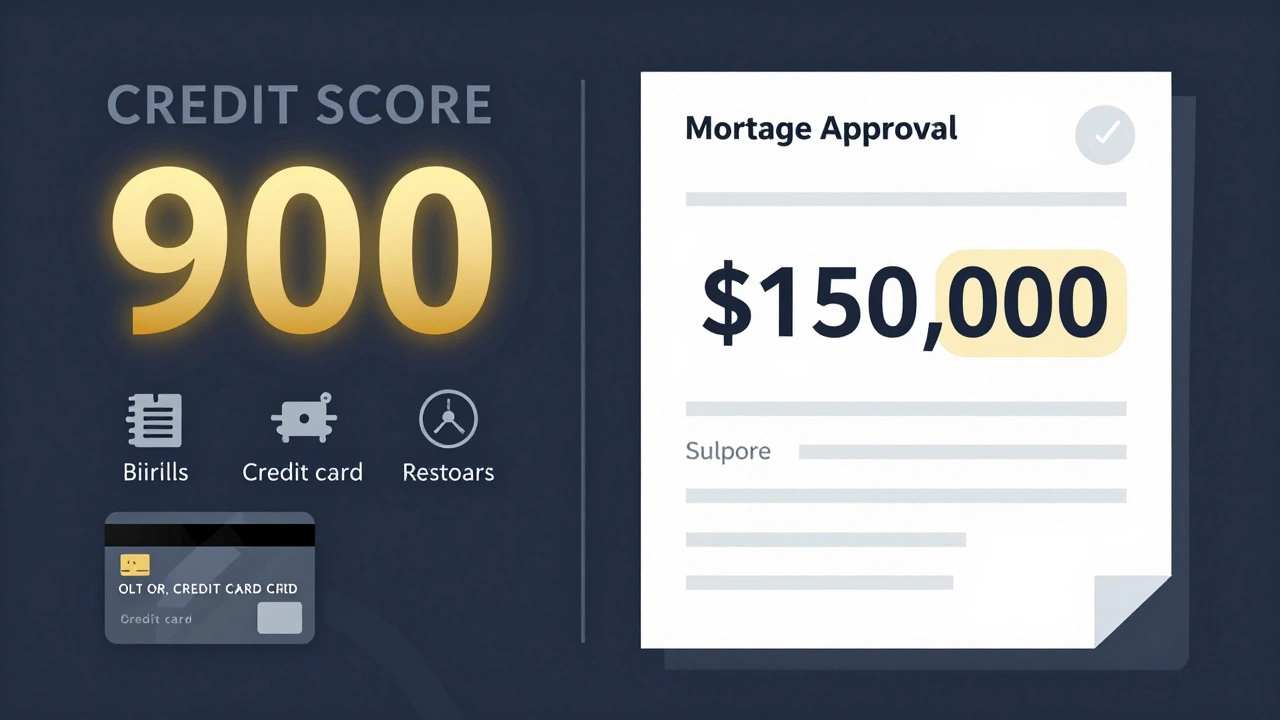

You’ve heard it whispered in real estate offices and shouted in online forums: 900 credit score. Is it real? Can you actually hit that number-and if you do, does it get you a better mortgage as a first-time buyer in New Zealand? The short answer is yes, a 900 credit score is possible. But here’s the truth most people don’t tell you: it doesn’t matter as much as you think.

What does a 900 credit score even mean?

In New Zealand, credit scores range from 0 to 1,200, depending on the agency. Equifax, illion, and Experian all use slightly different scales, but 900 is near the top of the range for most. That’s not just good-it’s elite. Only about 2% of New Zealanders hit 900 or above. You’ve paid every bill on time for years. You’ve never missed a payment. You’ve kept your credit card balances under 10% of your limit. You’ve had the same credit card for a decade. You’ve never applied for new credit unless you absolutely had to.

But here’s what no one says out loud: lenders don’t care if your score is 850 or 900. Once you’re in the ‘excellent’ range-which starts around 800 in most systems-you’ve already unlocked the best rates and terms. A 900 score doesn’t get you a lower interest rate than an 870. It doesn’t make your loan approval faster. It doesn’t give you extra cash back or a free home inspection. It just means you’re statistically unlikely to ever default. And that’s it.

How do you actually get to 900?

Getting to 900 isn’t about tricks. It’s about consistency over time. Here’s what it takes:

- Pay everything on time, every time. One late payment can drop you 100 points. Even a 15-day delay on a phone bill or gym membership can show up.

- Keep credit utilisation below 10%. If your limit is $10,000, spend no more than $1,000 per month. Pay it off before the statement date so the balance reported to the credit bureau is low.

- Don’t open new accounts. Every hard inquiry knocks a few points off. If you’re trying to hit 900, avoid credit cards, personal loans, or even mobile phone contracts for at least 12 months.

- Keep old accounts open. Your credit history length matters. Closing a 15-year-old credit card? That can erase years of history overnight.

- Use different types of credit. Having a mix-like a credit card, a car loan, and a home loan-helps. But if you don’t have a loan, don’t take one just to boost your score. It’s not worth the risk.

It takes at least five years of perfect behaviour to get close to 900. Most people who reach it are in their 40s or 50s. If you’re 25 and just starting out, aiming for 900 is like trying to run a marathon before you’ve learned to jog. Focus on 800 first. That’s where the real benefits kick in.

Does a 900 credit score help first-time buyers?

As a first-time buyer, your biggest hurdle isn’t your credit score. It’s your deposit. Even with a 900 score, you still need 10% to 20% of the home price saved up. In Auckland, that’s $100,000 to $200,000 on a $1 million house. No lender will give you a mortgage if you’ve got perfect credit but no savings.

What a high score does help with:

- Getting approved for a higher loan amount

- Accessing the lowest interest rates (usually 0.1%-0.3% lower than average)

- Being taken seriously by lenders when you have irregular income (like freelancers or gig workers)

But here’s the reality: most first-time buyers in New Zealand get approved with scores between 720 and 820. That’s the sweet spot. You don’t need 900. You need a steady job, a clean payment history, and a deposit. That’s it.

What lenders really look at

Behind the credit score, lenders dig into your bank statements, your employment history, your debts, and your spending habits. They want to know: Can you afford this house? Will you still pay if your car breaks down or your partner loses their job?

One client I worked with had a 910 score. He had $5,000 in savings and applied for a $700,000 home. He got rejected-not because of his credit, but because his monthly expenses ate up 90% of his income. His score didn’t save him.

Another had a 740 score, saved $150,000 over three years, worked full-time for five years, and had zero debt. He got approved for a $750,000 mortgage with the lowest rate on the market.

Your credit score is just one piece. Your income, your deposit, your job stability, and your spending habits matter more.

What’s the real advantage of a high credit score?

The real win isn’t the mortgage. It’s the freedom.

People with scores above 850 can get approved for credit cards with 0% balance transfers, better insurance rates, lower phone bills, and even faster rental approvals. They don’t need a guarantor. They don’t need to pay huge deposits for utilities. They can rent a car overseas without a credit card hold. They’re trusted by default.

For first-time buyers, that freedom means less stress. You can move faster when you find the right house. You don’t have to wait for a lender to request five extra documents. You’re not stuck waiting for a manual review.

But again-none of that replaces saving. A 900 score won’t buy you a house. Your savings will.

What should first-time buyers actually focus on?

Forget chasing 900. Focus on this:

- Save your deposit first. Aim for 10% minimum. If you’re in Auckland, start with $100,000. Use a KiwiSaver first-home withdrawal if you qualify.

- Check your credit report. Go to Equifax or illion and get your free report. Look for errors-old debts, duplicate accounts, or mistakes. Fix them before applying for a loan.

- Pay everything on time. Set up auto-pay for bills. Even if you can only afford the minimum, don’t miss a date.

- Don’t open new credit. No new credit cards. No personal loans. No ‘buy now, pay later’ apps like Afterpay or Zip if you’re planning to buy in the next 12 months.

- Keep your debt low. If you have student loans or car payments, make sure they’re under control. Lenders look at your debt-to-income ratio. If you owe $40,000 and earn $60,000, you’re already pushing your limits.

Do those five things, and you’ll be in the 800+ range without even trying. And that’s more than enough.

Myth: You need a perfect score to buy your first home

This myth is pushed by financial influencers who sell courses on ‘crushing your credit score.’ They make it sound like 900 is the golden ticket. It’s not. It’s a trophy. A nice one. But not the key to homeownership.

In 2025, 78% of first-time buyers in New Zealand got their mortgage with a score below 850. The average was 786. That’s not bad. That’s normal.

What’s not normal? Waiting five more years to chase 900 while rent keeps rising and prices climb another 15%. That’s the real cost.

Bottom line: Aim for 800. Save for 10%. Move.

A 900 credit score is possible. It’s impressive. But it’s not necessary. If you’re a first-time buyer, your time is better spent saving money than tweaking your credit utilisation by 2%.

Build your deposit. Fix your credit report. Pay your bills on time. Avoid new debt. That’s your path to homeownership. Not a perfect score. Not a magic number. Just steady, smart habits.

When you’re ready to buy, your credit score will be good enough. It always is.

Corbin Fairweather

I am an expert in real estate focusing on property sales and rentals. I enjoy writing about the latest trends in the real estate market and sharing insights on how to make successful property investments. My passion lies in helping clients find their dream homes and navigating the complexities of real estate transactions. In my free time, I enjoy hiking and capturing the beauty of landscapes through photography.

view all postsWrite a comment