BTL Profit Calculator

Property Details

Expense Details

Monthly Profit Summary

Buying a property to rent it out isn’t just about owning a home-it’s about building a steady income stream. That’s what BTL, or buy-to-let, is all about. You purchase a property, fix it up if needed, and then rent it to tenants. The rent you collect each month covers your mortgage, maintenance, and taxes, and ideally leaves you with some extra cash. Simple? Yes. Easy? Not always. But if you know how it works, you can make it work for you.

What Exactly Is BTL?

BTL stands for buy-to-let. It’s a type of property investment where you buy a home not to live in yourself, but to rent out to someone else. This isn’t flipping houses or short-term vacation rentals. It’s long-term renting, usually under an Assured Shorthold Tenancy (AST) in the UK, or similar agreements elsewhere. You become a landlord, and your tenant pays you monthly rent. The goal? To earn more in rent than you spend on the property each month.

Most people use a mortgage to buy BTL properties. Unlike a regular home loan, a BTL mortgage is based on the expected rental income, not just your personal salary. Lenders want to see that the rent will cover at least 125% of your monthly mortgage payment. That’s a safety buffer. If your tenant moves out or the rent goes down, you still have room to breathe.

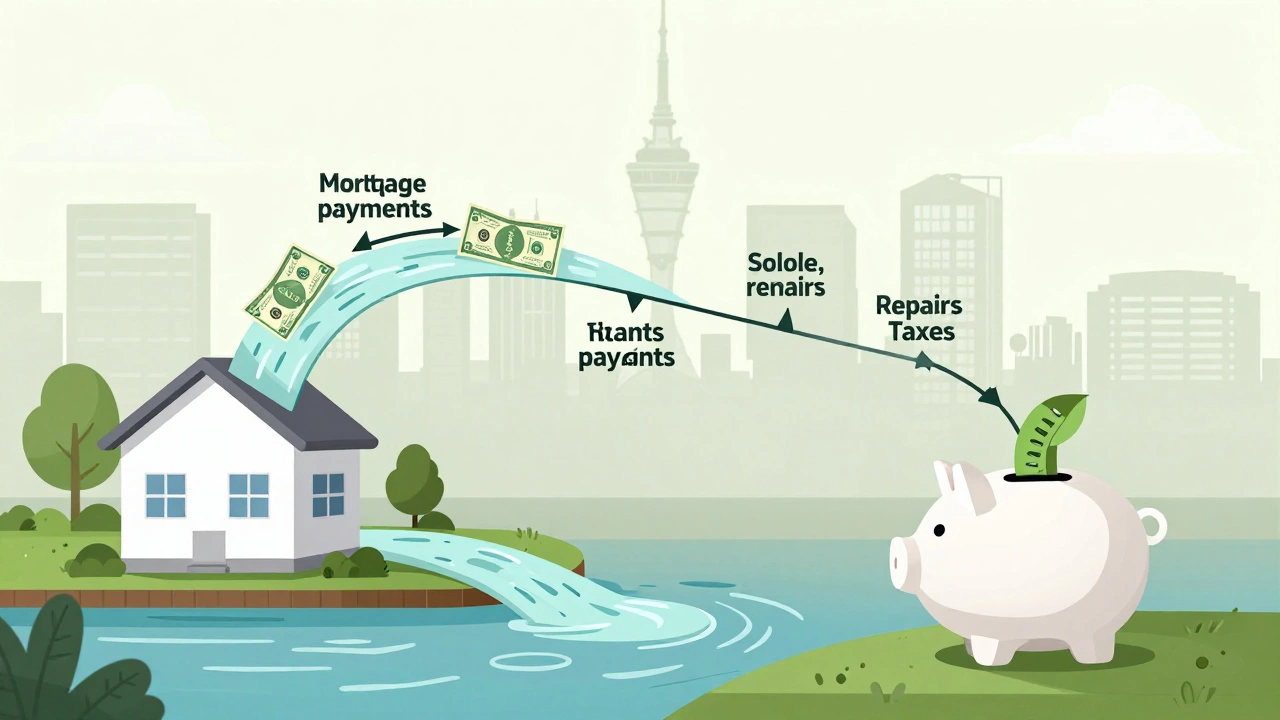

How Does the Money Flow?

Let’s say you buy a two-bedroom flat in Auckland for $650,000. You put down 25% ($162,500) and borrow the rest. Your BTL mortgage rate is 6.8%, so your monthly payment is around $3,100. You find a tenant willing to pay $3,800/month in rent. That gives you $700 left over each month after the mortgage.

But that’s not the whole picture. You also have to pay:

- Property management fees (if you use an agent: 8-12% of rent)

- Building insurance (around $1,200/year)

- Council rates and water charges ($400-$800/year)

- Maintenance and repairs (plumbing, electrical, painting-budget $100-$300/month)

- Void periods (when the unit is empty between tenants)

After all that, your net profit might be $200-$400/month. Not life-changing, but it adds up. Over five years, that’s $12,000-$24,000 in cash flow, plus the property’s value may rise. In Auckland, property values have grown about 5-7% annually over the last decade. That means your flat could be worth $850,000 in five years-even if you don’t get a single dollar in rent.

Who Is BTL For?

BTL isn’t for everyone. It’s not a get-rich-quick scheme. You need:

- Some savings for the deposit and upfront costs

- A stable income to qualify for the mortgage

- Patience-tenants don’t always pay on time, and repairs don’t wait

- Willingness to deal with bureaucracy: tenancy agreements, inspections, tax filings

Many BTL investors start after they’ve paid off their own home. Others use equity from their primary residence. A growing number are young professionals who can’t afford to buy their own place but still want to get into property. They rent out a studio or one-bedroom unit while living with roommates.

It’s also popular among people planning for retirement. Rent from a BTL property can become a reliable income stream when your salary stops.

Taxes and Rules You Can’t Ignore

Landlords pay tax on rental profit. In New Zealand, you must declare all rent you receive. You can deduct expenses like mortgage interest, repairs, insurance, and agent fees. But you can’t deduct your own time or the cost of improvements like a new kitchen-those are capitalized and depreciated over time.

There’s also the Bright-Line Test. If you sell a residential property within 10 years of buying it, you may owe capital gains tax-unless it’s your main home. That means if you buy a BTL property and sell it in three years, you’ll likely owe tax on the profit. Wait five years? Still taxable. Wait ten? Maybe not. The rules change, so always check with an accountant.

There are also rules around tenant rights. You can’t just evict someone because you want to sell. You need a valid reason-non-payment, damage, or you need the property back for yourself. And you have to give proper notice (usually 90 days). Skipping these rules can cost you money in legal fees or compensation.

Where to Find Good BTL Properties

Not all areas are equal. A $500,000 house in a quiet suburb might sit empty for months. But a $450,000 apartment near a university, train station, or hospital? That’s in demand. Look for:

- Proximity to public transport

- Good schools (even if you’re not renting to families)

- Low crime rates

- Areas with population growth

In Auckland, suburbs like Mt Roskill, Onehunga, and Mangere have strong rental demand because they’re affordable and well-connected. Avoid areas with too many new developments-oversupply drives down rent. Check local council data on population trends and rental vacancy rates. You’ll find this on Stats NZ or local council websites.

What Can Go Wrong?

Every investment has risks. BTL is no different.

- Void periods: Tenants leave. It takes time to find new ones. Budget for 4-6 weeks of lost rent per year.

- Bad tenants: Some don’t pay, damage the property, or refuse to leave. A good tenancy agreement and a bond (usually 4 weeks’ rent) help. But you still need to go through the Tenancy Tribunal if things go south.

- Interest rate hikes: If your mortgage rate jumps from 6.8% to 8%, your profit shrinks fast. Fixing your rate for 3-5 years can protect you.

- Market crash: If property values drop 15%, you’re still okay if you’re holding long-term and cash flow is positive. But if you need to sell, you could lose money.

The key? Don’t rely on property value rising. Rely on rent covering costs. If rent doesn’t cover your mortgage and expenses, you’re not investing-you’re subsidizing.

Is BTL Still Worth It in 2026?

Yes-but only if you’re smart about it. Interest rates are still higher than they were in 2020. The market isn’t booming like it did during the pandemic. But demand for rental housing is stronger than ever. More people can’t afford to buy. More young adults are staying in rentals longer. Remote work means people move more often, and they need flexible housing.

Here’s what’s changed:

- BTL mortgages are harder to get. Lenders are stricter about income verification.

- Tax rules are tighter. You can’t claim as many deductions as before.

- More investors are entering the market, so competition is higher.

But here’s the upside: rental yields in Auckland are still around 4-5%. That’s higher than most savings accounts, term deposits, or even some shares. And unlike stocks, you can see and touch your asset. You can improve it. You can control it.

If you’re willing to do the work-find the right property, screen tenants, manage repairs, stay on top of taxes-BTL can be one of the most reliable ways to build long-term wealth. It’s not glamorous. But it works.

Do I need a real estate agent for BTL?

You don’t need one, but it helps. An agent can find tenants faster, handle inspections, collect rent, and manage repairs. They typically charge 8-12% of monthly rent. If you’re new to BTL or have a full-time job, using an agent saves stress. If you’re hands-on and live nearby, you can manage it yourself to keep more profit.

Can I use my superannuation to fund a BTL property?

In New Zealand, you can’t use KiwiSaver funds to buy a BTL property. KiwiSaver can only be used for your first home, and only if you haven’t owned one before. You can’t use it to invest in rental property. You’ll need to save separately or use equity from another property.

What’s the minimum deposit for a BTL mortgage?

Most lenders require at least 20-30% down. Some might accept 15% if you have strong income and credit, but those are rare. A 25% deposit is the standard. The more you put down, the lower your monthly payments and the better your chances of approval.

How long should I hold a BTL property?

At least 5-7 years. That’s how long it usually takes to break even after upfront costs like legal fees, inspections, and renovations. After 7 years, you start seeing real returns from both rent and property growth. Selling before then often means you lose money due to transaction costs and tax.

Are BTL properties a good investment in Auckland right now?

Yes, if you choose wisely. Auckland still has one of the highest rental demands in New Zealand. While prices are higher than in 2020, rents have also risen. The key is to focus on areas with strong tenant demand-not just the cheapest property. A well-located, well-maintained unit will always find tenants, even in a slower market.

Corbin Fairweather

I am an expert in real estate focusing on property sales and rentals. I enjoy writing about the latest trends in the real estate market and sharing insights on how to make successful property investments. My passion lies in helping clients find their dream homes and navigating the complexities of real estate transactions. In my free time, I enjoy hiking and capturing the beauty of landscapes through photography.

view all postsWrite a comment