Joint Ownership Risk Assessment Tool

Assess Your Joint Ownership Risk

Answer these questions to determine if joint ownership is right for you.

What Joint Ownership Actually Means

In a joint ownership set‑up, each party is a co‑owner someone who holds an equal, undivided interest in a property. The default rule in many jurisdictions, including NewZealand, is that the ownership is joint tenancy-meaning the right of survivorship applies: if one owner dies, their share automatically passes to the surviving owner(s), bypassing the will.

This sounds convenient, but it also means you lose control over what happens to your share. Any change-sale, mortgage, or legal claim-requires the consent of all owners.

Major Risks of Joint Ownership

Below are the most common headaches that have driven lawyers and financial planners to advise against joint ownership for most buyers.

1. Credit and Debt Exposure

Because the property is a shared asset, a default on a mortgage the loan taken out to purchase or refinance a property by any co‑owner drags down the credit rating of everyone involved. In 2023, the NewZealand Credit Bureau reported a 12% rise in joint‑mortgage defaults linked to divorce and business failures.

2. Lack of Autonomy

Deciding to sell or refinance requires unanimous consent. If one party moves overseas or decides to keep the property, the others can be stuck with a property they no longer want or can’t afford.

3. Legal Disputes

Disagreements over maintenance, rent collection, or improvement costs often end up in the Family Court. A single lawsuit can freeze the title deed the legal document that proves ownership of real estate, preventing any sale until the dispute resolves.

4. Inheritance Complications

Since the right of survivorship overrides a will, a parent who co‑owns with a child can unintentionally disinherit other heirs. Moreover, if a joint owner dies intestate, the surviving owners inherit automatically, which may clash with the deceased’s estate plan.

5. Tax and Property Tax Issues

Joint owners are each liable for their share of property tax. If one fails to pay, the tax authority can place a lien on the entire property, jeopardising all owners’ equity.

Comparing Ownership Models

Choosing the right structure is a balancing act between flexibility, protection, and tax efficiency. The table below highlights the core differences.

| Feature | Joint Tenancy | Tenancy in Common | Sole Ownership |

|---|---|---|---|

| Right of Survivorship | Yes | No - shares pass via will | Not applicable |

| Equal Shares Required | Usually yes | No - can be unequal | N/A |

| Decision to Sell | Unanimous consent | Any owner can force sale via court | Owner alone decides |

| Credit Exposure | Shared across all owners | Shared only for the portion owned | None from other parties |

| Tax Treatment | Income split equally | Income split by ownership % | All income to single owner |

Alternatives That Offer More Control

Tenancy in common a form of co‑ownership where each party holds a distinct share that can be transferred or bequeathed independently is the most popular alternative. It keeps the right of survivorship out of the picture, letting each owner decide how their portion is dealt with after death.

Another route is to keep the property under a trust a legal entity that holds assets for the benefit of beneficiaries. A trust can own the title deed, and you can be the beneficiary. This isolates personal assets from co‑owner risk and simplifies inheritance.

For couples, a prenuptial or postnuptial agreement that spells out what happens to the property in case of separation can mitigate many joint‑ownership pitfalls.

How to Safeguard an Existing Joint Ownership

If you’re already in a joint ownership set‑up, you don’t have to jump ship immediately. Here’s a practical playbook:

- Draft a written co‑ownership agreement. Include provisions for:

- How expenses and improvements are split.

- What happens if one owner wants out.

- Procedures for handling a default on a mortgage.

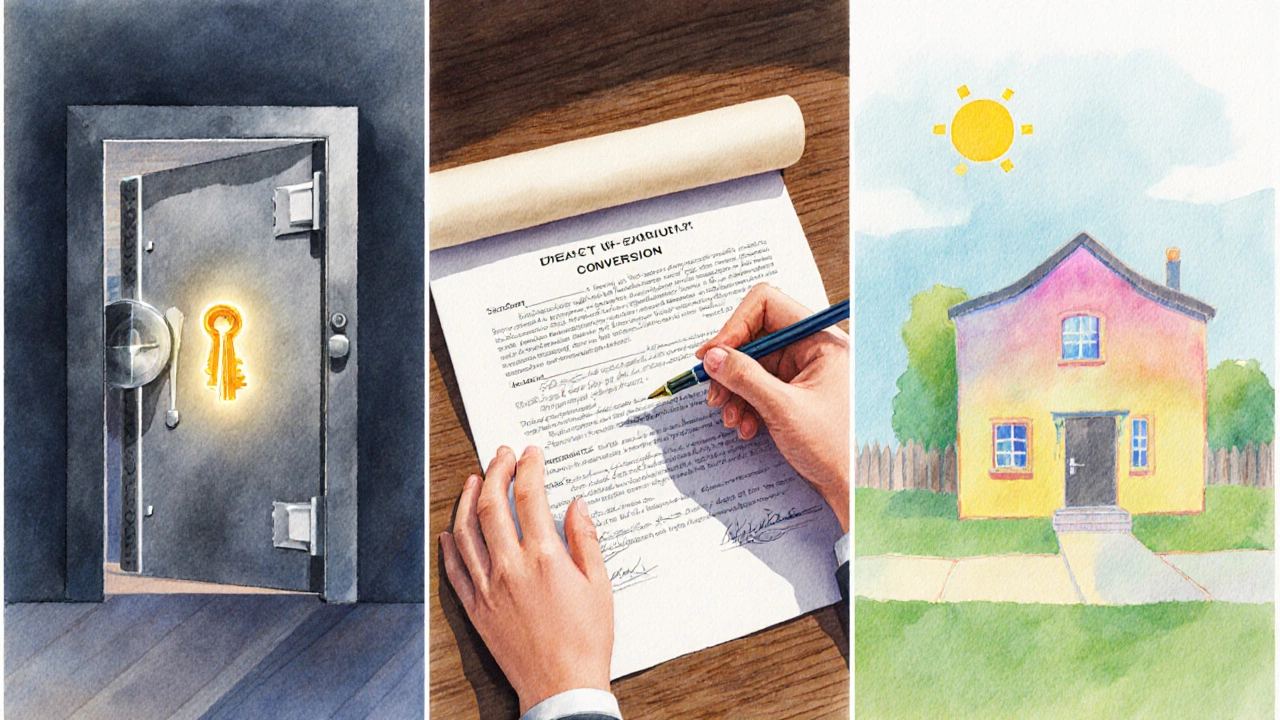

- Register a deed of variation a formal amendment to the title that records changes in ownership interests with Land Information NewZealand (LINZ). This makes the agreement legally binding.

- Consider converting the joint tenancy to a tenancy in common. A simple filing with LINZ can split the shares, allowing each owner to treat their portion as a separate asset.

- Secure personal insurance and a separate life insurance policy that names the other co‑owner as a beneficiary for the owner’s share. This prevents the property from becoming a contested estate.

- Review the property’s property tax the annual levy charged by the local council based on property value obligations annually to ensure all owners are up to date.

Decision Checklist: Is Joint Ownership Right for You?

- Do you trust the other party to meet mortgage payments for the next 10‑15 years?

- Is your relationship (personal or business) stable enough to withstand major life changes?

- Have you considered the tax impact of splitting rental income or capital gains?

- Do you have a clear exit strategy documented in a co‑ownership agreement?

- Would separating ownership (tenancy in common or trust) provide more flexibility for inheritance?

If you answered “no” to more than one of these, it’s worth exploring an alternative structure before signing the next title deed.

Common Questions About Joint Ownership

Can I sell my share of a jointly owned property?

Only if all co‑owners agree. Otherwise, you may need to apply to the court for a partition sale, which can be costly and time‑consuming.

What happens to the property if a joint owner dies?

Under joint tenancy, the surviving owner(s) automatically inherit the deceased’s share, regardless of any will. This is known as the right of survivorship.

Is joint ownership the same as a partnership?

No. A partnership is a legal business entity with its own tax ID, whereas joint ownership is simply a way of holding title. Partnerships can own property, but they bring separate tax and liability rules.

Can I convert joint tenancy to tenancy in common?

Yes. In NewZealand, you can file a deed of variation with LINZ to split the shares. Once converted, each owner can bequeath their portion independently.

How does joint ownership affect my credit score?

If a joint mortgage is in default, all owners are reported as delinquent, which can lower each person’s credit rating. Even a single missed payment can affect every co‑owner.

In short, joint ownership can feel like a shortcut to buying a home, but the hidden legal and financial ties often outweigh the convenience. By weighing the risks, exploring alternatives, and locking in a solid co‑ownership agreement, you protect not just your property, but your future.

Corbin Fairweather

I am an expert in real estate focusing on property sales and rentals. I enjoy writing about the latest trends in the real estate market and sharing insights on how to make successful property investments. My passion lies in helping clients find their dream homes and navigating the complexities of real estate transactions. In my free time, I enjoy hiking and capturing the beauty of landscapes through photography.

view all postsWrite a comment