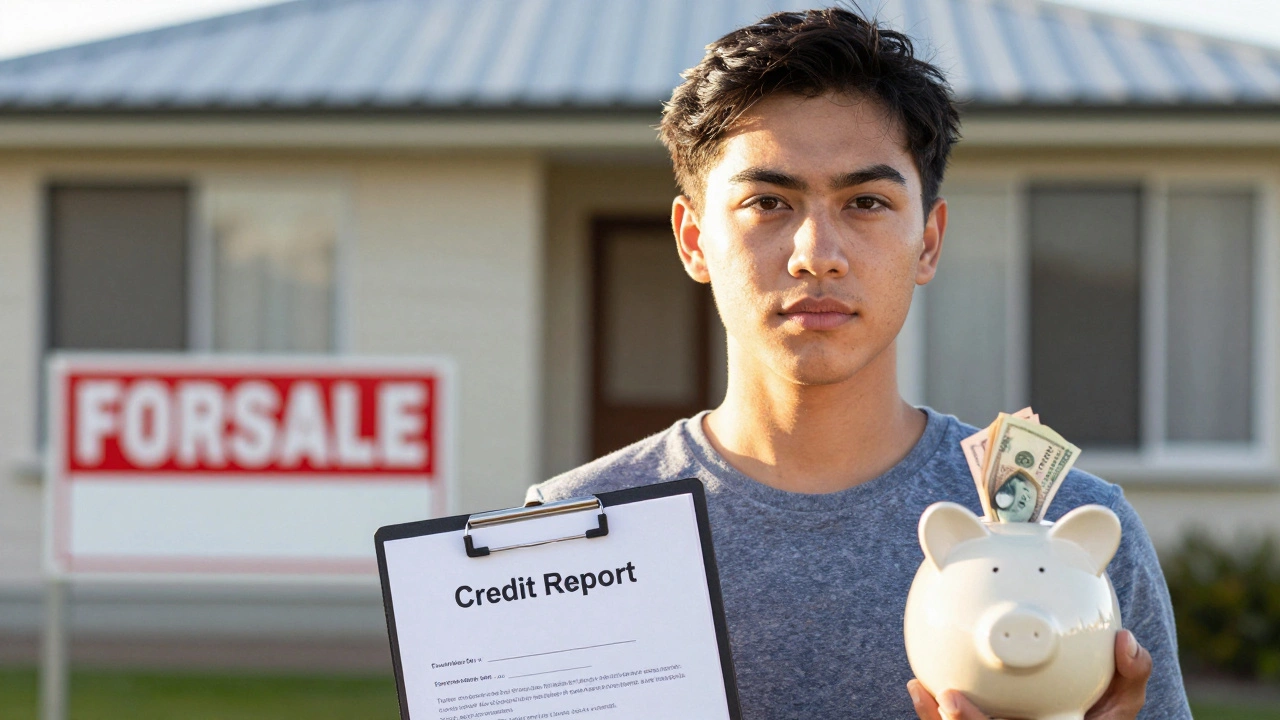

When people talk about a perfect credit score, a credit rating typically above 750 that signals low risk to lenders. Also known as excellent credit, it’s the golden ticket to the best mortgage deals, lower interest rates, and higher loan limits. But here’s the truth: you don’t need a perfect score to buy a home. Many first-time buyers close on houses with scores in the 650s. What matters more is how your score fits with your income, debt, and down payment.

That’s why lenders don’t just look at your credit score, a three-digit number based on your borrowing history, payment behavior, and credit usage. They also check your debt-to-income ratio, the percentage of your monthly income that goes toward paying debts like loans and credit cards. If you earn $5,000 a month and owe $2,000 in payments, that’s a 40% ratio—most lenders want it under 43%. Your down payment, the upfront cash you put toward a home purchase also plays a huge role. Put down 20%? You might get approved even with a 680 score. Put down 3%? Then your score better be 720 or higher.

And it’s not just about numbers. Lenders look at your payment history. Did you miss a payment last year? Did you max out your cards? Did you open five new accounts in six months? These red flags can sink your application faster than a low score. On the flip side, steady payments over time—even with a modest score—can build trust. That’s why some buyers with 670 scores get better deals than others with 740 scores: it’s not just the number, it’s the story behind it.

The posts below cover real cases: how much you can borrow with a 650 score, what lenders demand for a $2 million home, and why FHA loans feel harder than they should. You’ll find practical breakdowns of shared ownership, first-time buyer programs in Virginia and New Zealand, and how estate agents use credit info to guide buyers. No fluff. No theory. Just what actually works when you’re trying to get a mortgage in today’s market.