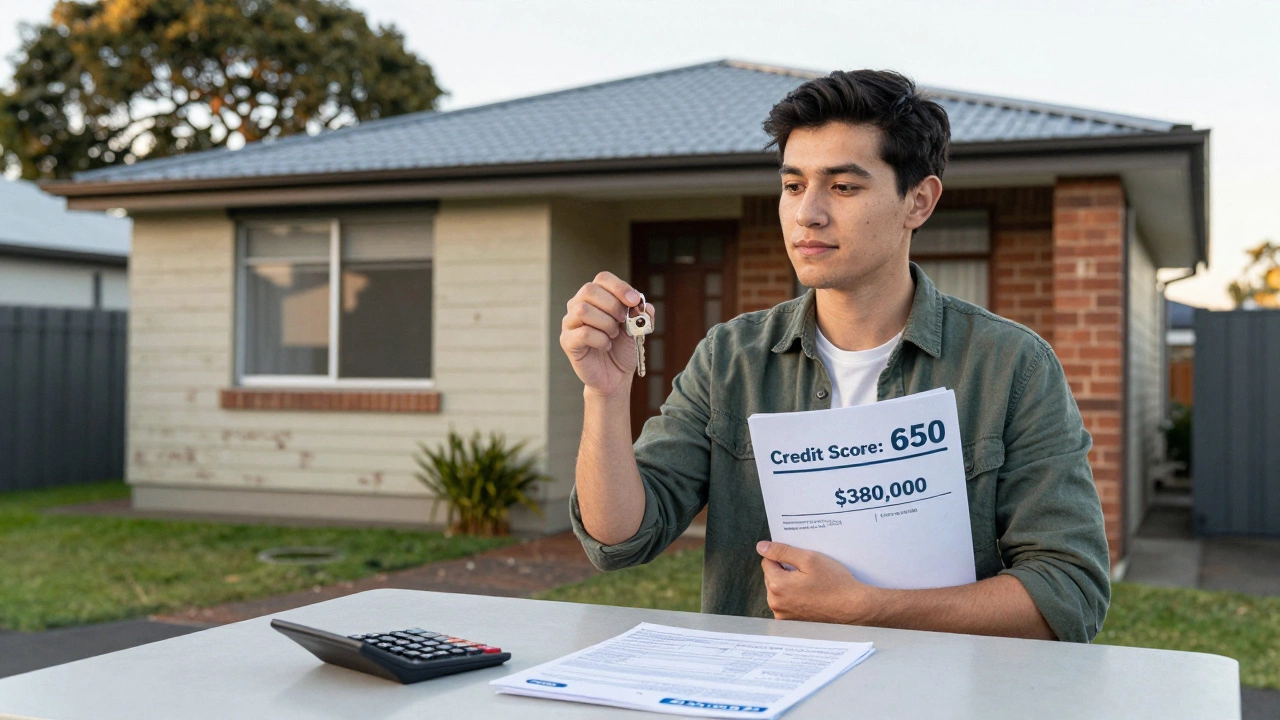

Getting a mortgage with poor credit, a home loan approved despite a low credit score or past financial mistakes. Also known as a bad credit mortgage, it’s harder—but far from impossible—if you know what lenders care about beyond the number on your report. Most people think a credit score below 600 shuts the door, but that’s not true. Lenders look at your whole story: how much you earn, how steady your job is, how big your down payment is, and whether you’ve paid bills on time lately. A low score doesn’t mean you’re out of the game—it just means you need to play smarter.

One big thing people miss? down payment, the upfront cash you put toward a home purchase. Cash reserve matters more than you think when your credit is shaky. Putting down 10% or 20% can make lenders overlook a 580 score if you’ve got steady income and no recent late payments. Even if you can’t afford a huge down payment, programs like FHA loans in the UK (and similar schemes) let you get in with as little as 5% down—if you’ve cleaned up your credit habits. And yes, credit repair, the process of fixing errors and building positive payment history. credit rebuilding, is real. Paying off small debts, disputing mistakes on your report, and staying current for six months can move your score enough to qualify. You don’t need a 750 score to buy a home. You just need to prove you’re not a risk right now.

Some lenders specialize in mortgage with poor credit, a home loan approved despite a low credit score or past financial mistakes. bad credit mortgage. They’re not shady—they’re just focused on different metrics. They’ll look at your bank statements, your rental history, even your utility bills. If you’ve paid rent on time for two years straight, that counts. If you’ve got a steady job and no new debt, that helps too. You might pay a bit more in interest, but that’s better than renting forever. And if you’re thinking about shared ownership, a way to buy part of a home while paying rent on the rest. part-buy, part-rent, that’s another path. It lowers the upfront cost and can be easier to qualify for with a weaker credit history.

Don’t believe the myth that you need perfect credit to own a home. Thousands of people with credit scores under 600 bought homes last year. They didn’t wait for perfection. They focused on what they could control: saving more, paying bills on time, and finding lenders who actually understand real life. Below, you’ll find real stories, real advice, and real options—from how to raise your score fast to which lenders still work with people who’ve had bankruptcies or missed payments. This isn’t about fixing your past. It’s about building your future, one step at a time.