When it comes to home loan eligibility, the set of financial and personal criteria lenders use to decide if you can borrow money to buy a home. Also known as mortgage approval requirements, it’s not just about your credit score—it’s about your whole financial picture. Many people think a high credit score is the golden ticket, but that’s only one piece. Lenders also look at your income stability, how much debt you already have, and whether you’ve saved enough for a down payment. If you’re aiming to buy in the UK, especially in high-cost areas like London or Manchester, the bar can feel higher than ever.

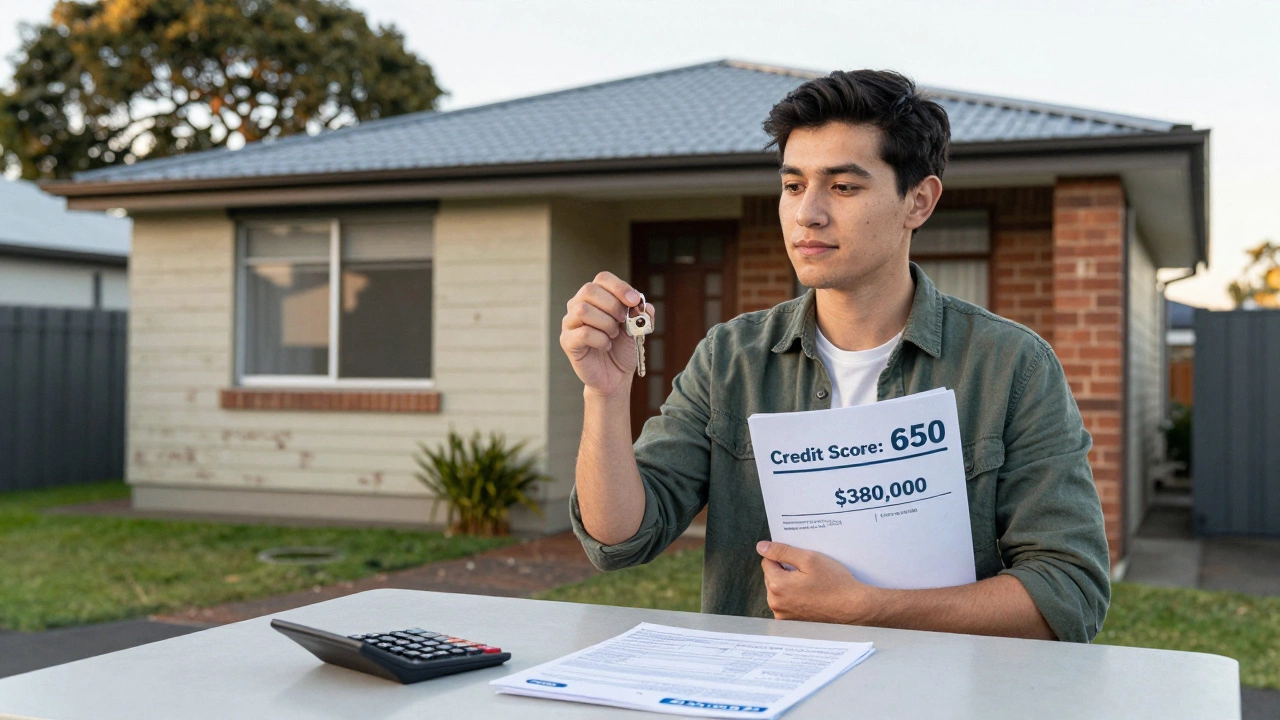

One major factor is down payment requirements, the upfront cash you need to pay before the lender covers the rest of the home price. In the UK, most lenders want at least 5% to 10%, but first-time buyers often use government schemes like Help to Buy to reduce that. Then there’s credit score for home loan, a number lenders use to judge how risky you are as a borrower. You don’t need a perfect 850—many UK lenders approve applicants with scores above 620, as long as they’ve paid bills on time for the last year. But if you’ve missed payments, maxed out cards, or have too many recent credit applications, that’ll hurt your chances.

Another thing people overlook is debt-to-income ratio, how much of your monthly income goes toward paying off loans and credit cards. If you’re paying £800 a month on car loans and student debt, and you earn £3,000, lenders will see you as stretched thin—even if your credit score is solid. They want to make sure you can still afford the mortgage after covering everything else. That’s why some buyers get turned down even when they’ve saved a big deposit. It’s not just about what you have—it’s about what you owe and how steady your income is.

First-time buyers often think they need to wait until they’ve saved a huge amount or cleared all debt. But that’s not true. Many people qualify with modest savings and a steady job. The key is knowing what lenders care about—and fixing what you can before you apply. You might not need a perfect score. You might not need 20% down. But you do need to show you’re responsible with money. That’s what really matters.

Below, you’ll find real guides from buyers who’ve been through it—whether they were on a £40k salary in Auckland, navigating shared ownership in the UK, or trying to get approved with a credit score under 700. These aren’t theory pieces. They’re practical, no-fluff breakdowns of what worked, what didn’t, and what lenders actually said yes to.