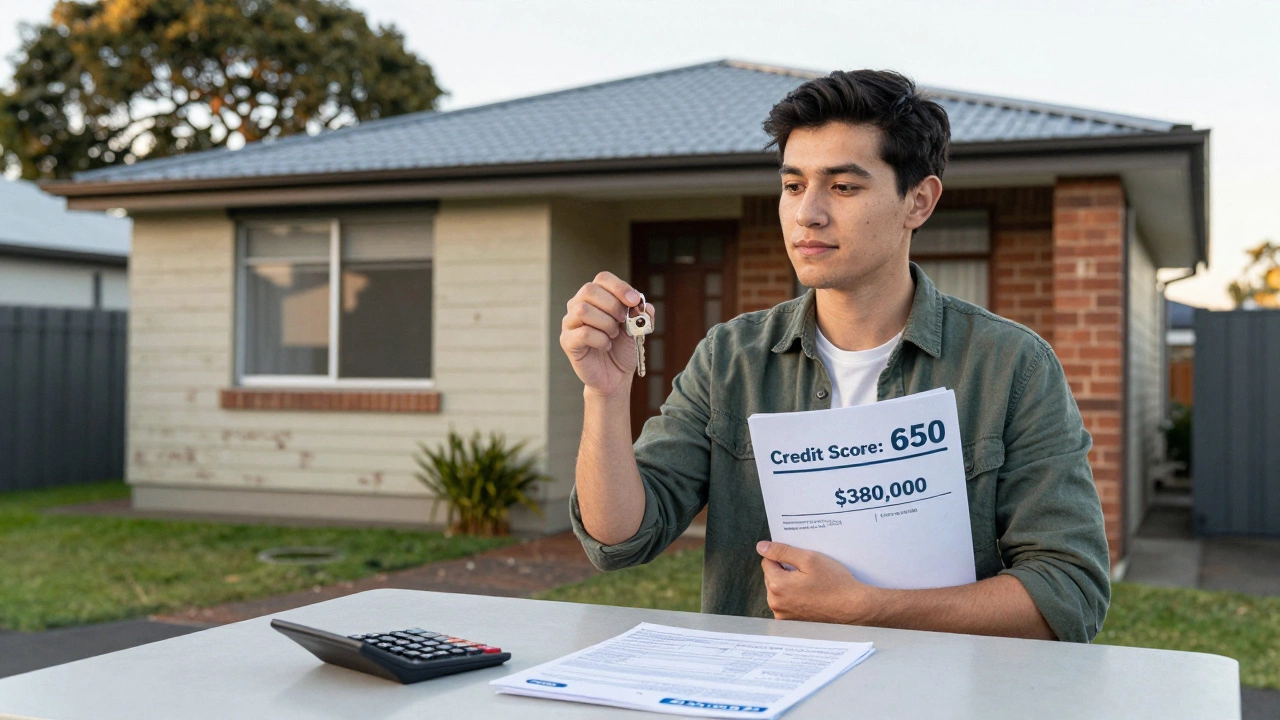

When you're buying your first home, a first time buyer loan, a mortgage product designed for people who haven't owned a home before. Also known as first-time buyer mortgage, it’s not a magic solution—it’s a tool that works only if you understand how it fits with your income, savings, and long-term goals. Most people think these loans are easier to get, but the truth is, lenders still care about your credit score, how much you can put down, and whether you can afford the monthly payments. You don’t need a 900 credit score to qualify, but you do need to show you pay bills on time and aren’t drowning in debt. In the UK, programs like Help to Buy and shared ownership are often mixed into this conversation, but they’re not the same thing. Help to Buy gives you a government loan to boost your deposit, while shared ownership lets you buy a portion of a home and pay rent on the rest. Both are designed to get you in the door, but they come with strings attached.

One thing most first-time buyers miss is that the loan is just the start. You also need to think about down payment assistance, programs that help cover part of your upfront cash needed to buy a home. In places like London or Manchester, even a 5% deposit can mean £20,000 or more. That’s why many turn to family help, government schemes, or even shared ownership to reduce the upfront cost. But here’s the catch: if you go with shared ownership, you’re not fully owning your home. You’re owning a share—say, 25% or 50%—and paying rent on the rest. That rent can go up, and when you want to sell, you might have to pay fees to the housing association. It’s not a trap, but it’s not a free pass either. You need to know how shared ownership, a system where you buy part of a property and rent the remainder from a housing association works before you sign anything. And if you’re on a low income, like £40k a year, you’ll need to know which areas still have affordable options and what grants you might qualify for.

There’s no single path. Some buyers use FHA-style loans (though those are US-based), others use Help to Buy, and some just save longer and go conventional. What works in Virginia won’t always work in Manchester. The key is matching your situation to the right option. You’ll find posts here that break down exactly how much you need for a £100,000 home, what credit score actually matters, and how to talk to an estate agent without getting pushed into something you can’t afford. You’ll also see real talk about shared ownership pitfalls, how staircasing works, and why some landlords still won’t let you have a pet—even if you’re a perfect tenant. This isn’t theory. It’s what people actually run into when they try to buy their first home in the UK. Read through the posts below, find what matches your situation, and skip the fluff. You’ve got a home to buy. Let’s get you there.