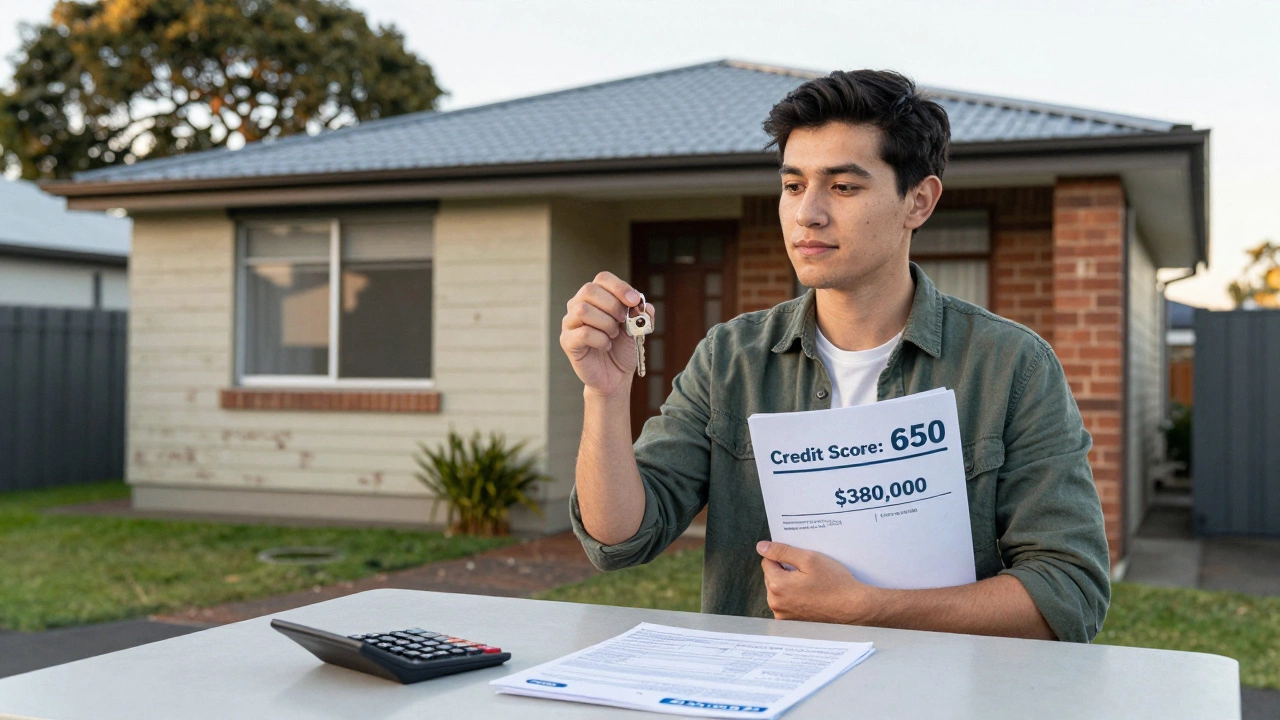

When you're applying for a credit score, a three-digit number that tells lenders how likely you are to repay debt on time. Also known as credit rating, it’s the first thing a lender checks before even looking at your income or savings. A high score doesn’t guarantee you’ll get approved, but a low one can shut the door before you even start. Most lenders in the UK want at least a 620, but if you’re aiming for the best rates, you’ll need 700 or higher. It’s not magic—it’s math based on your payment history, how much you owe, and how long you’ve had credit.

That mortgage, a long-term loan used to buy property, with the home itself serving as collateral. isn’t just about how much you can borrow—it’s about how much it’ll cost you over 25 years. A 650 credit score might get you a 5.5% interest rate. A 760? You could drop to 4.1%. That’s thousands in savings over the life of the loan. And no, you don’t need a perfect 850. You just need consistent, on-time payments, low credit card balances, and no recent missed bills. Lenders care more about your behavior over the last 12 months than your lifetime record.

Many first-time buyers think they need a huge deposit to qualify, but that’s not always true. Some schemes let you put down as little as 5%, but your credit score has to be rock solid. If your score is shaky, a bigger deposit won’t fix it. On the flip side, if your score is strong, even a small down payment can work. The real barrier isn’t money—it’s trust. Lenders trust people who pay bills on time, keep debt low, and don’t open new accounts right before applying.

You’ll also see mentions of first-time home buyer programs. These aren’t handouts—they’re tools. They often require you to complete homebuyer education, stick to income limits, and use approved lenders. But they don’t lower your credit score requirement. If anything, they make it stricter because they’re designed for people who are financially responsible but can’t afford a full purchase yet.

What you won’t find in most guides? The truth that your credit score matters more than your salary. A person earning £30,000 with a 780 score can often get better terms than someone earning £60,000 with a 600 score. That’s because lenders don’t just look at how much you make—they look at how you manage what you have. Missed payments, maxed-out cards, or too many loan applications in six months? That’s a red flag, no matter how high your income.

And don’t get tricked by ads promising to fix your score overnight. You can’t game the system. The only real way to improve it? Pay everything on time, reduce what you owe, and wait. It takes months, not days. But if you start now, you could be in a much better position in a year.

Below, you’ll find real advice from people who’ve been through it—how to check your score for free, what to do if you’ve got a mistake on your report, why some lenders ignore scores above 750, and how shared ownership programs use credit checks differently. No fluff. Just what works.