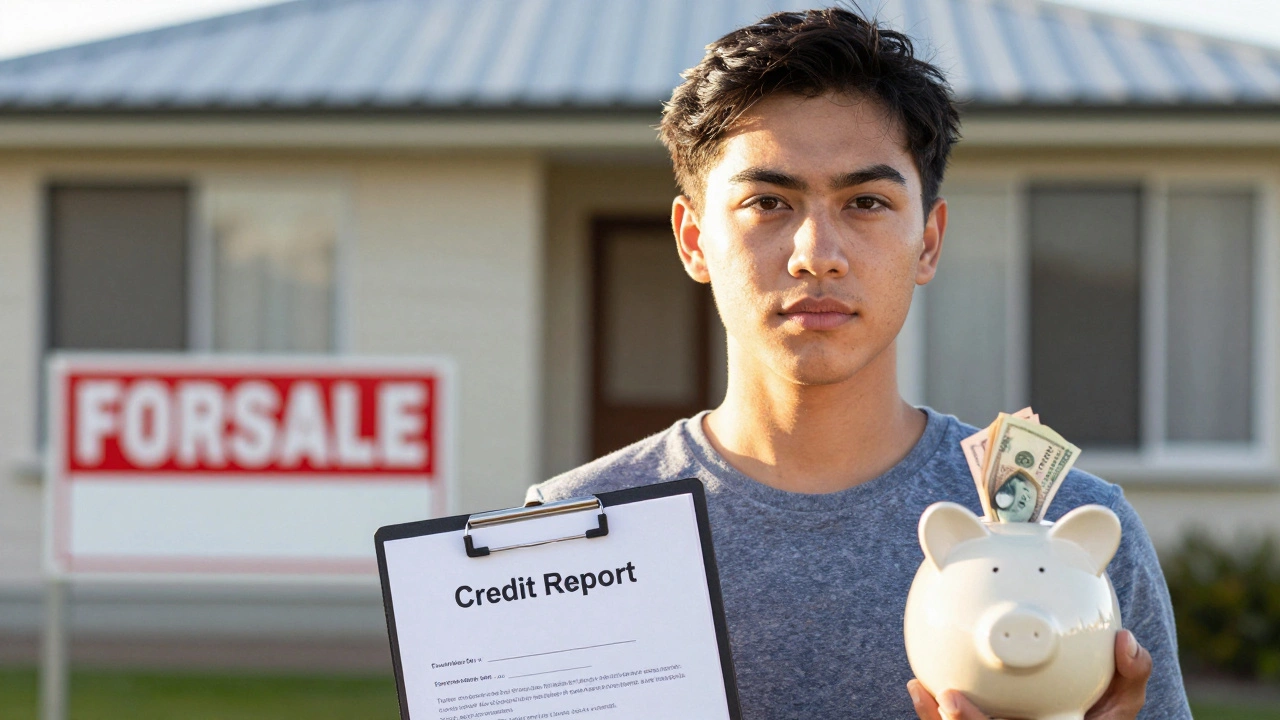

When you're looking to buy a home in New Zealand, your credit rating NZ, a numerical measure of your borrowing reliability based on your payment history, debt levels, and credit activity. Also known as credit score, it’s the first thing lenders check before even looking at your income. A score of 650 might get you approved, but it won’t get you the best deal. Lenders in Auckland, Wellington, and Christchurch use this number to decide if you’re a safe bet—and how much risk they’re taking by lending you tens of thousands of dollars.

Your credit score, a three-digit number that reflects how responsibly you’ve managed debt over time isn’t just about missing payments. It’s also about how much you owe compared to what you can borrow, how long you’ve had credit accounts, and how often you apply for new loans. If you’ve got a first-time buyer NZ, a person purchasing their first home, often relying on government schemes and low-deposit options status, lenders might give you a little more room—but only if your credit history shows stability. A score below 600? You’ll struggle to find a lender willing to work with you without a huge deposit or a co-signer. A score above 700? Suddenly, you’re in the running for lower rates and bigger loans.

It’s not just about numbers. Your home loan NZ, a mortgage secured against property in New Zealand, typically requiring proof of income, deposit, and creditworthiness approval also depends on your job stability, existing debts, and whether you’ve got savings tucked away. Even with a great score, if you’re juggling car payments, credit cards, and student loans, lenders will see you as stretched thin. That’s why people with solid credit ratings but high debt still get turned down. The real key? Keep your debts low, pay everything on time, and avoid applying for new credit in the six months before you apply for a mortgage.

And here’s something most first-time buyers don’t realize: your credit rating affects more than just the loan amount. It controls your interest rate, which can save or cost you tens of thousands over the life of your mortgage. A 1% difference in rate on a $500,000 loan? That’s over $100,000 in extra payments. That’s why checking your credit rating NZ early—and fixing errors—isn’t just smart, it’s essential. You can get a free report from Equifax or Illion. Look for late payments you didn’t make, accounts you didn’t open, or old debts that should’ve been removed. Fix those, and you’re not just improving your score—you’re improving your future.

Below, you’ll find real advice from people who’ve been there: how much you can borrow with a 650 score, what lenders actually look for beyond the number, how shared ownership changes the game, and why some buyers on $40k a year still end up with keys in hand. No fluff. Just what works in today’s NZ market.